Property managers have added more screening vendors, more income checks, and more process controls over the last few years.

But one fragile trust assumption still survives in many leasing workflows: if an applicant uploads a bank statement that looks normal, the team may start using it before anyone verifies whether the file itself was manipulated.

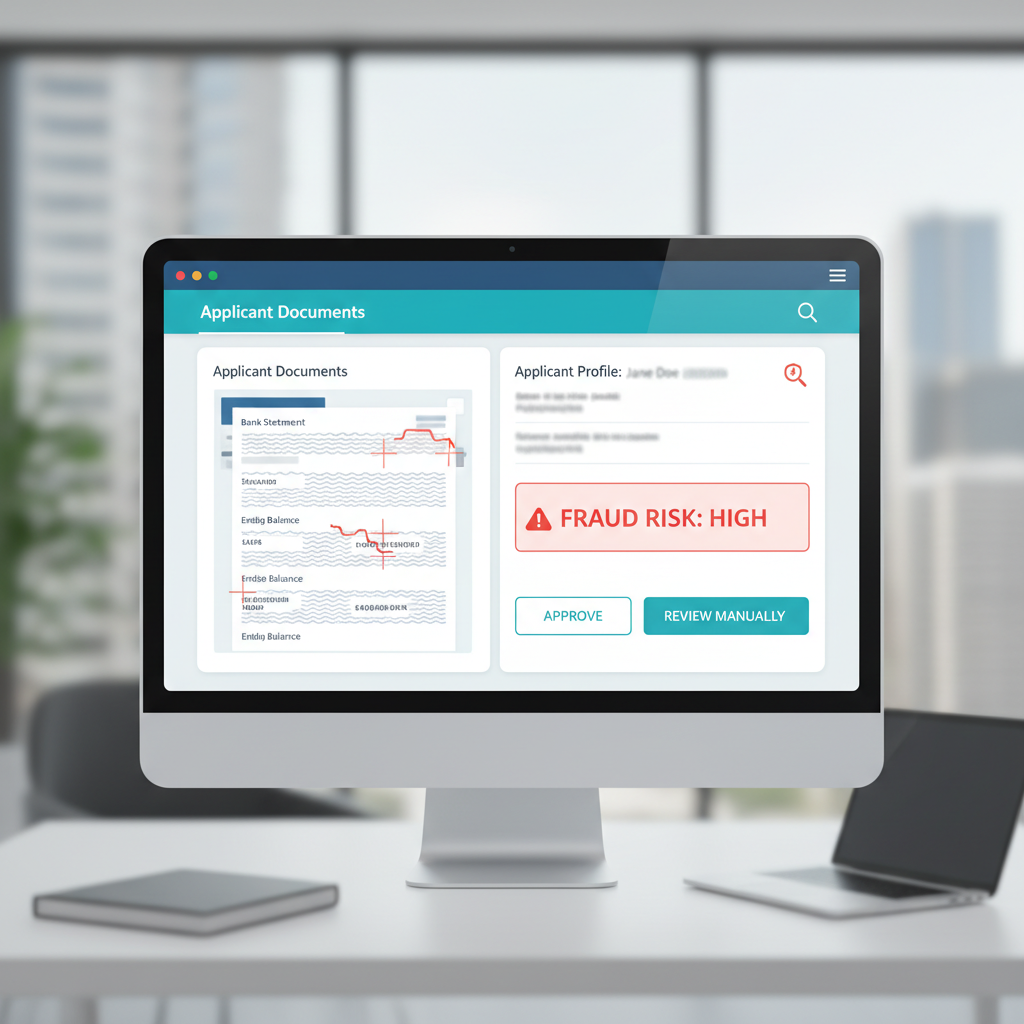

The missing step: many tenant-screening workflows validate the applicant story, but not the authenticity of the uploaded bank statement document.

That matters more in 2026 because rental fraud is rising, AI-generated application documents are easier to produce, and leasing teams are under pressure to approve quickly without introducing friction for legitimate applicants.

Why This Problem Is Growing in Multifamily Leasing

Recent multifamily risk reporting makes the direction clear. Risk Management Magazine, citing National Apartment Association and National Multifamily Housing Council research, reported in April 2026 that more than 70% of respondents to a 2024 NMHC survey saw fraudulent applications and payments increase over the prior 12 months. The same write-up notes that owners are seeing AI-generated pay stubs, phony bank statements, and fabricated IDs at the earliest screening stage.

That matters because the initial application review is still where a lot of trust gets assigned. Once a file looks coherent, the workflow starts moving around it.

Why Leasing Teams Still Ask for Bank Statements

Even when a property uses payroll connections, employment verification, or third-party screening, uploaded bank statements still show up constantly in rental applications.

They help answer questions like:

- does the applicant appear to have enough liquidity to cover deposits, move-in costs, or reserve expectations?

- does recent account activity support the stated income story?

- are there recurring deposits that look consistent with the application?

- does the file make sense for self-employed or non-standard earners?

- should the application move forward when other income evidence is partial or mixed?

If the uploaded statement is false, every downstream judgment about affordability and reliability starts on the wrong foundation.

What Existing Tenant-Screening Controls Usually Miss

Leasing teams already do real work. They run background checks, review pay stubs, contact employers, screen identities, and compare disclosed income against rent thresholds.

Those controls are valuable, but they usually answer questions like:

- does the applicant meet the property's income standard?

- is there enough documented cash flow to justify approval?

- does the identity and employment story hold together?

- should this application proceed to lease approval?

They do not automatically answer the narrower question that matters first:

Was this bank statement altered before upload?

A forged statement can still contain plausible balances, consistent math, and clean OCR output. That is exactly why document authenticity needs its own control layer.

What Fraudsters Actually Change on a Rental Application Statement

The file does not need to look fake. It only needs to remove one leasing objection.

That can mean:

- raising ending balances to suggest stronger reserves

- editing deposit amounts to make income look more stable

- removing overdrafts or negative events that make the applicant look riskier

- changing account-holder details to connect a stronger account to the applicant

- submitting a screenshot or re-exported PDF that hides earlier edits behind normal-looking compression

In each case, the leasing decision shifts because the document changed, not because the applicant's real financial position improved.

Where Bank Statement Verification Belongs in Tenant Screening

The most useful place is near document intake, before the statement becomes trusted evidence inside the application file.

- Applicant uploads bank statement through portal, email, or leasing intake flow

- Document verification runs on the file itself before balances are trusted

- Clean files continue to screening, underwriting-style review, or exception handling

- Suspicious files route to manual escalation before the property relies on them for approval

- Only then should the statement influence affordability confidence, reserve analysis, or lease approval

This is the same sequencing logic strong lending and AP teams are learning elsewhere: verify the evidence file first, then let extraction, review, and decisioning build on top of it.

Why OCR, Income Checks, and Manual Review Are Not Enough

OCR helps because it extracts what the statement says. Employment and payroll checks help because they validate parts of the applicant story. Human reviewers help because they can catch inconsistencies and context problems.

None of those controls are a document-forensics layer by default.

If a PDF has been edited cleanly, OCR may read the altered values perfectly. If a screenshot was re-saved after manipulation, a reviewer may just see a familiar bank layout and plausible balances. If the rest of the file looks orderly, the process usually calms down around the statement too early.

That is the operational risk. The workflow starts treating the uploaded statement as evidence before the file has earned that status.

What DocVerify Can Credibly Check Here

Based on the current product and codebase, DocVerify fits this intake step because it already analyzes PDFs and common image uploads, the same formats property teams routinely receive from applicants.

Relevant signals for rental statement review include:

- PDF structural anomalies that do not match a normal statement origin

- metadata irregularities that suggest editing or re-export chains

- font provenance and glyph anomalies around altered text regions

- occluded or hidden text analysis where overlays may conceal changes

- recompression artifacts in screenshots and image-based submissions

- model-based tamper localization that points reviewers toward suspicious areas

That does not replace employment verification, credit screening, or bank-linking products when those are available. It closes the earlier gap where an uploaded statement becomes trusted simply because it is present and readable.

A Better Rule for Property Managers

If a bank statement is important enough to support a lease decision, it is important enough to verify before it shapes the file.

- clean document + consistent applicant story + normal screening review → continue

- suspicious document → escalate before approval

- uncertain file provenance → do not let extraction accuracy substitute for trust

That is the practical shift. Do not ask only whether the statement supports the application. Ask whether the statement itself deserves to be used as evidence.

Rental Screening Needs a Trust Layer Too

Leasing teams are moving faster, which makes document trust more important, not less. A smoother portal, stronger OCR, or a better applicant score does not make an uploaded bank statement authentic.

If your rental workflow still accepts applicant-uploaded financial documents, bank statement verification belongs before leasing confidence compounds around them.

- Try DocVerify: https://docverify.app

- Broader bank statement fraud angle: Fake Bank Statements in Lending and Rental

- Related income-document risk: Fake Pay Stubs in Lending and Rental