Auto lenders have added more fraud controls, more income checks, and more automated decisioning over the last few years.

But one fragile trust assumption still survives in a lot of files: if a borrower uploads a bank statement that looks normal, the workflow may start using it before anyone verifies whether the file itself was manipulated.

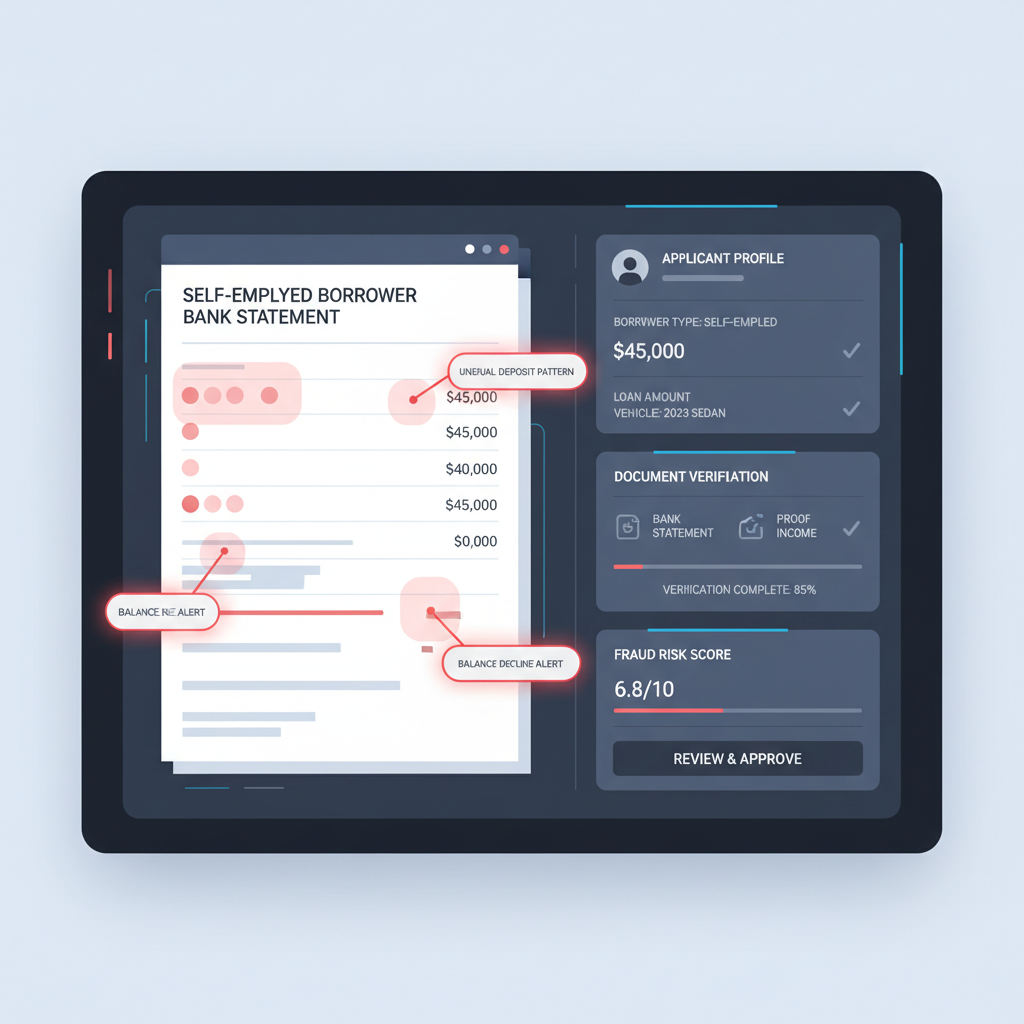

The missing step: many auto lending workflows validate the applicant story, but not the authenticity of the uploaded bank statement document.

This matters most when the borrower is self-employed, works on commission, has gig income, or otherwise falls outside a clean payroll-based proof-of-income path. In those files, the bank statement often becomes the trust anchor.

Why This Matters in Auto Lending Right Now

Point Predictive's 2025 fraud reporting on auto lending found that total auto lending fraud risk reached $9.2 billion in 2024, with income and employment misrepresentation accounting for about $3.9 billion, or 42% of the total. That is the biggest single fraud category in the stack.

Not every one of those losses starts with a fake bank statement. Many start with false employment details, fake pay stubs, or inflated stated income. But in edge-case underwriting, especially for self-employed borrowers, uploaded bank statements still become a critical piece of evidence for whether the income story feels believable enough to approve.

That is exactly why the document itself deserves verification before the workflow compounds confidence around it.

Why Bank Statements Still Show Up in Auto Loan Files

For W-2 borrowers with straightforward payroll, lenders may rely more heavily on pay stubs, employer verification, tax returns, or direct data connections.

But for a meaningful share of real-world files, underwriters still ask for bank statements because they help answer questions like:

- does deposit activity support the claimed income pattern?

- does the borrower appear to have stable cash flow over time?

- are there enough reserves to reduce early-default risk?

- do personal and business cash flows make sense for a self-employed borrower?

- should the file proceed when other proof-of-income documents are thin, delayed, or inconsistent?

When the uploaded statement is edited, the workflow does not just inherit a bad document. It inherits false confidence about affordability.

The Underwriting Gap Is Not the Same as the Income-Calculation Gap

Auto lenders already spend real effort on proof of income. They compare stated income to bureau data, review pay stubs, check debt ratios, inspect application consistency, and escalate suspicious files.

Those steps matter. But they usually answer questions like:

- is the borrower likely able to make the payment?

- does the employment or business story hold together?

- are the deposits consistent enough to support the stated income?

- does the file meet underwriting policy?

They do not automatically answer the narrower question that comes first:

Was this uploaded bank statement altered before it entered the underwriting file?

A forged statement can still have plausible balances, realistic deposit cadence, and perfectly readable OCR output. That is exactly why extraction and authenticity need to be treated as separate controls.

What Fraudsters Actually Change on Auto-Loan Bank Statements

The goal is usually not to fabricate an entire financial life. It is to remove one underwriting objection.

That can mean:

- inflating recurring deposits to make income look more stable

- raising ending balances to imply stronger reserves

- removing overdrafts or reversals that make the file look riskier

- editing account-holder or business-name fields so the statement appears to match the borrower better

- submitting a screenshot or re-exported PDF that hides the edit trail behind a normal-looking file

In each case, the underwriting decision changes because the document changed, not because the borrower's real financial condition improved.

Where Bank Statement Verification Belongs in Auto Lending

The most useful place is at document intake, before the uploaded statement becomes trusted input for proof-of-income review or final approval.

- Borrower uploads bank statement through dealership flow, lender portal, or follow-up conditions process

- Document verification runs on the file itself before deposits and balances are trusted

- Clean files continue into income assessment, exception handling, and underwriting review

- Suspicious files route to fraud or manual escalation before they shape the approval decision

- Only then should the statement influence affordability confidence, deal structure, or stip resolution

That sequencing matters because downstream review is calmer once the statement is inside the file. If the first trust decision is wrong, the rest of the process often gets easier for the fraudster.

Why OCR, Manual Review, and Policy Controls Still Miss This

OCR helps because it extracts what the statement says. Policy controls help because they enforce process discipline. Manual review helps because experienced underwriters notice context problems.

None of those controls are a document-forensics layer by default.

If a screenshot was edited cleanly, OCR may read the altered numbers perfectly. If a PDF was re-exported after selective changes, the file may still look consistent to a reviewer under time pressure. If the deposit pattern looks plausible, a lender can move on to affordability logic without asking whether the evidence file itself earned trust.

That is the operational trap. The workflow starts treating a readable document as a reliable document.

What DocVerify Can Credibly Check Here

Based on the current product and codebase, DocVerify is well matched to this intake problem because it already supports PDFs and common image uploads, including screenshot-style document submissions.

Relevant signals for auto-loan bank statement review include:

- metadata anomalies such as edit-history and suspicious software markers

- font mismatch and text-layer inconsistencies in altered fields

- clone and tamper signals where content may have been duplicated or patched

- recompression and screenshot patterns that show a re-saved or re-captured workflow

- model-based suspicious-region localization that points reviewers to where the file deserves closer attention

That does not replace direct bank linking, employment verification, or other fraud vendors. It closes the narrower but important gap where an uploaded statement becomes trusted simply because it is present, coherent, and easy to read.

A Better Rule for Auto Underwriters

If a bank statement is important enough to support approval, it is important enough to verify before it shapes the file.

- clean document + consistent income story + normal underwriting review → continue

- suspicious document → escalate before approval

- uncertain file provenance → do not let extraction accuracy substitute for trust

This is especially important in self-employed and exception-heavy auto lending, where one uploaded file can materially change whether a borrower appears financeable.

Auto Lending Needs a Document Trust Layer Too

Auto lending fraud is not only a stated-income problem or a synthetic-identity problem. It is also a document-trust problem.

If your workflow still accepts borrower-uploaded bank statements, bank statement verification belongs before underwriting confidence compounds around them.

- Try DocVerify: https://docverify.app

- Related income-document risk: Fake Pay Stubs in Lending and Rental

- Related W-2 fraud angle: Fake W-2 Forms and Income Fraud

- Broader bank statement fraud angle: Fake Bank Statements in Lending and Onboarding