The $40 Billion Problem Nobody Talks About

Bank statements are the bedrock of financial trust. Lenders use them to underwrite mortgages. Property managers use them to screen tenants. Fintechs use them to onboard customers. Insurance companies use them to validate claims.

And right now, anyone with a browser can generate a pixel-perfect fake in under sixty seconds.

AI-generated document fraud increased 5x in 2025 alone. Deloitte estimates that generative AI could push U.S. fraud losses to $40 billion annually by 2027. The most common target? Financial documents — bank statements, pay stubs, and tax returns — the exact documents that lending, rental, and onboarding workflows treat as ground truth.

The core problem: every pipeline that accepts a bank statement PDF or screenshot and extracts numbers from it is making a trust assumption that no longer holds.

How Fake Bank Statements Actually Work

Forget the old days of clumsy Photoshop edits. Modern bank statement fraud operates at three levels of sophistication:

Level 1: Template generators

Websites and Telegram bots sell bank statement templates for major institutions. The user fills in their name, account number, and desired balances. The output is a clean PDF with correct fonts, logos, and formatting. Cost: $5 to $50.

Level 2: AI-assisted editing

Users upload a real bank statement and use AI tools to modify specific values — ending balances, deposit amounts, transaction descriptions. The edits are pixel-consistent with the original document. The metadata, fonts, and layout remain intact. These are extremely difficult to catch visually.

Level 3: Fully synthetic generation

Generative AI models produce entire bank statements from scratch. They replicate institution-specific formatting, transaction patterns, running balances, and even the subtle visual artifacts of a scanned document. The output has never passed through a real bank's systems.

All three levels produce documents that pass manual review. Most pass OCR extraction without triggering any alerts. The numbers are internally consistent. The layouts are correct. The only thing missing is authenticity.

Where the Damage Lands

Mortgage and lending

U.S. lenders lose an estimated $1–2 billion annually to mortgage fraud, and the real number is significantly higher when unreported cases are included. Australia's Commonwealth Bank recently uncovered over $1 billion in suspected loan fraud involving AI-generated documentation — bank statements, pay stubs, and identity documents that passed traditional verification.

The pattern is consistent: applicants inflate balances, fabricate income deposits, or remove debt-related transactions to qualify for loans they cannot service. The lender's OCR pipeline extracts the numbers cleanly, the underwriting model approves the application, and the fraud only surfaces months later when payments stop.

Rental screening

Approximately 1 in 8 rental applications now contains some form of fraud. At large property management companies, up to 40% of applications vetted each month are fraudulent. The most common method: altered bank statements and fabricated pay stubs.

The downstream cost is severe. Applicants with fraudulent documents are 7 times more likely to end in eviction or incur bad debt. The average property management company writes off $4.2 million in bad debt annually, with roughly a quarter tied directly to fraud-related nonpayment.

Key statistic: 85% of property managers report being targeted by application fraudsters, up from 66% pre-pandemic. Altered documentation is the number one challenge, cited by 84% of respondents.

Customer onboarding and KYC

Fintechs, neobanks, and insurance companies routinely accept bank statement uploads during onboarding for income verification, proof of address, or account validation. When these documents are fabricated, the entire downstream relationship is built on false premises — credit limits are set too high, coverage is mispriced, and risk models operate on phantom data.

Why Traditional Checks Fail

Most organizations rely on one or more of these verification methods. None of them catch modern bank statement fraud reliably.

Manual review

A human reviewer looks at the document for obvious signs of tampering — misaligned text, wrong fonts, blurry regions. This worked when fraud required Photoshop skills. It does not work when AI generates documents that are visually indistinguishable from originals. Manual review also does not scale: a mortgage processor handling hundreds of applications per week cannot spend ten minutes inspecting every bank statement at the pixel level.

OCR and data extraction

OCR reads the text on the document and extracts structured data. It tells you what the document says. It does not tell you whether the document is real. A perfectly forged bank statement with correct formatting and consistent numbers will produce clean, valid OCR output. The extraction is accurate — the document is not.

Cross-referencing and logic checks

Some systems check whether the numbers on a bank statement are internally consistent — do the transactions add up to the ending balance? Is the running total correct? Modern fraud tools generate internally consistent documents by default. The math checks pass because the fraudster started with the desired ending balance and worked backward.

Open banking and direct feeds

Direct bank connections (via Plaid, Yodlee, or open banking APIs) bypass the document entirely by pulling data straight from the institution. This is the gold standard when available — but it is not always available. Many applicants cannot or will not connect their accounts. Some institutions do not support API access. International documents are rarely covered. And in many workflows, a PDF upload is still the primary intake method.

The Missing Layer: Document Authenticity

The gap in every one of these approaches is the same: none of them verify whether the document itself is genuine before acting on its content.

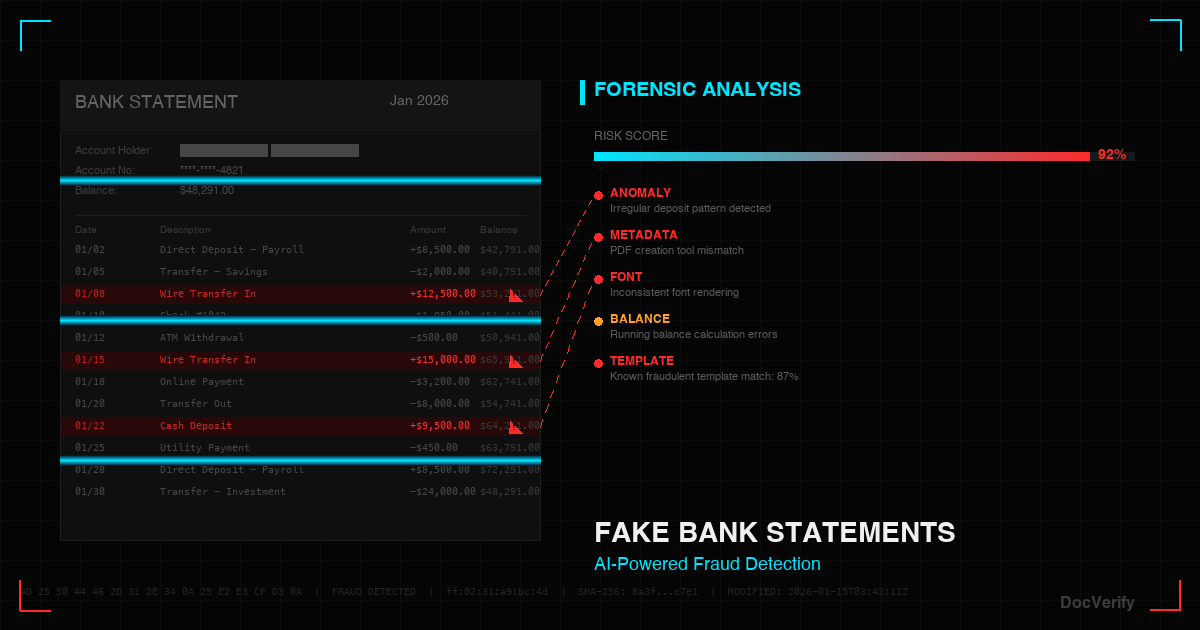

Document authenticity verification operates at the pixel level, below the text layer that OCR reads. It detects:

- Manipulation artifacts — subtle inconsistencies in compression, noise patterns, and rendering that appear when regions of a document have been edited

- Synthetic generation signatures — patterns characteristic of AI-generated content that differ from documents produced by real banking systems

- Metadata inconsistencies — mismatches between the document's claimed origin and its actual creation pipeline

- Visual anomalies — font rendering differences, alignment shifts, and color-space artifacts that are invisible to the human eye but detectable by forensic models

This is not a replacement for OCR, open banking, or manual review. It is the layer that should run before any of them.

The correct order of operations: verify the document is authentic → then extract its content → then make decisions based on that content. Skipping step one means every subsequent step operates on potentially fraudulent data.

What a Trust-First Pipeline Looks Like

Here is how organizations should structure their document intake:

- Document upload — applicant submits bank statement (PDF, image, or screenshot)

- Authenticity check — document passes through forgery detection before any data is extracted. Flagged documents are routed to manual review or rejected

- Data extraction — OCR or IDP extracts structured data from verified documents only

- Logic validation — cross-referencing, balance checks, and income calculations run on trusted data

- Decision — underwriting, approval, or onboarding proceeds with confidence that the source material is genuine

This architecture does not slow down the pipeline. Authenticity checks run in seconds. What it does is prevent the entire downstream workflow from operating on fabricated inputs.

The AI Agent Problem

This matters even more when AI agents are in the loop. Modern lending and property management platforms increasingly use AI copilots to summarize applications, flag risks, and recommend decisions.

If an AI agent processes a forged bank statement, it will:

- Extract the fake numbers accurately

- Summarize the fabricated financial position confidently

- Recommend approval based on data that does not exist

- Move the application downstream faster than a human reviewer ever would

AI agents are excellent at processing documents. They are not designed to question whether those documents are real. Without an authenticity layer, AI automation becomes an accelerant for fraud — making bad decisions faster and at greater scale.

Where DocVerify Fits

DocVerify provides the document-level authenticity check that sits before extraction, before agent processing, and before decisions.

For bank statement verification specifically, DocVerify screens uploaded documents for manipulation signals, synthetic generation patterns, and forensic anomalies — returning a trust score before your pipeline ever reads a single number from the document.

- Use it in lending pipelines to screen bank statements before underwriting models process them

- Use it in rental screening to flag manipulated financial documents before lease approval

- Use it in onboarding flows to verify document authenticity before setting credit limits or coverage

- Use it with AI agents so copilots only summarize and recommend based on verified source material

Get Started

If your pipeline accepts bank statement uploads and makes decisions based on what those documents say, you need to verify that the documents are real before you trust their content.

- Try DocVerify: https://docverify.app

- Learn about OCR vs. verification: Why extraction is not enough

- See invoice fraud patterns: How edited PDFs slip through AP automation

- Building agent workflows? Set up DocVerify with Claude Code MCP